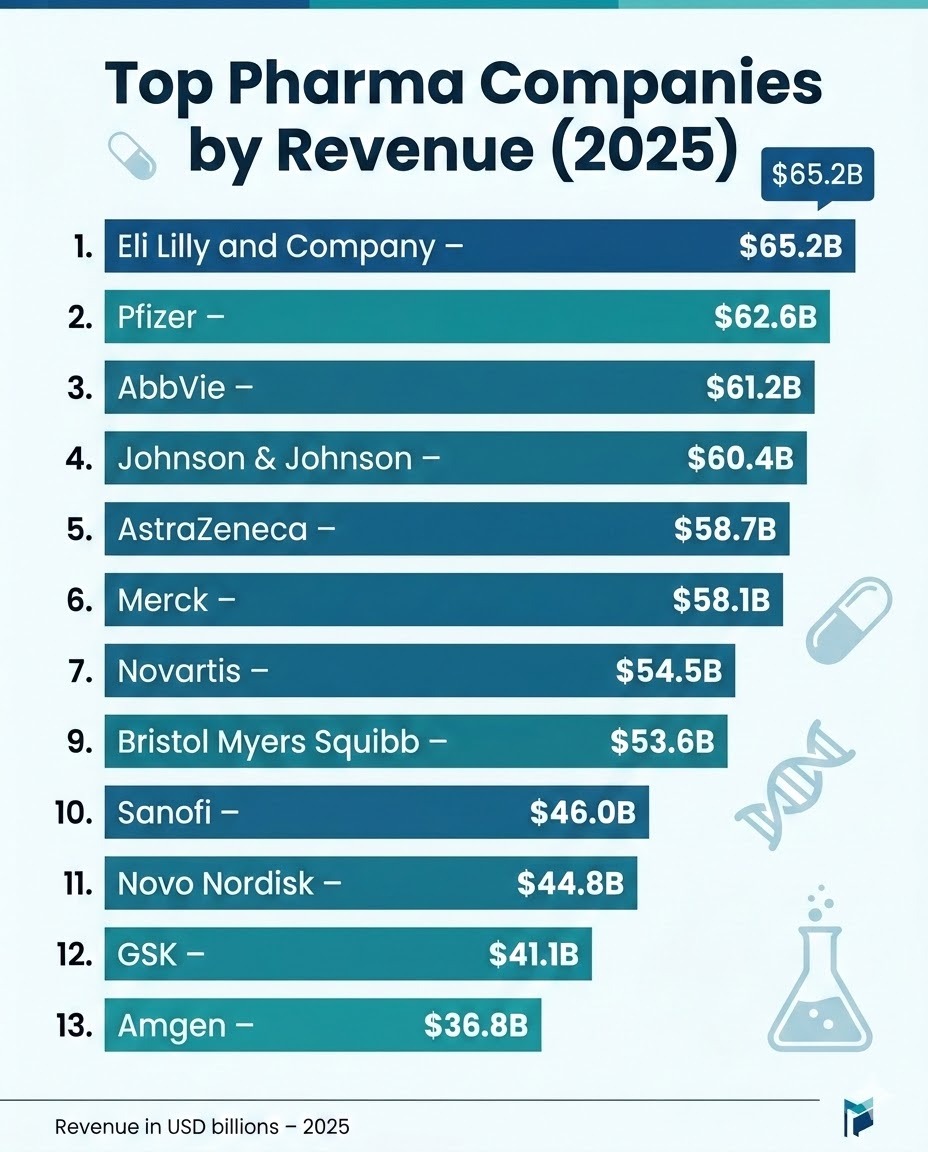

Eli Lilly hit $65.2 billion in revenue in 2025, beating everyone else. Most of that growth came from Mounjaro and Zepbound, their GLP-1 drugs for diabetes and weight loss. Nobody else is growing like this right now.

Pfizer is at $62.6 billion, AbbVie at $61.2 billion, and J&J at $60.4 billion. The gap between first and fourth is under $5 billion. That’s competitive.

AstraZeneca and Merck are almost tied at $58.7 billion and $58.1 billion. Both make cancer drugs, and that market still pays. AstraZeneca doesn’t have anything as big as Keytruda, but their portfolio is deep enough to keep them profitable.

Novartis and Roche are the European players, at $54.5 billion and $53.6 billion respectively. Both have solid cancer portfolios and other stuff that keeps them in the game. Roche has diagnostics too, which helps.

Bristol Myers Squibb is at $48.2 billion, Sanofi at $46.0 billion, and Novo Nordisk at $44.8 billion. BMQ is still sorting out the Celgene deal. Sanofi has been a mess for years. Novo Nordisk is smaller but making more money per dollar because of the GLP-1 boom—which is its own problem when the market saturates.

GSK is at $41.1 billion and Amgen at $36.8 billion. GSK spun off its consumer business and is trying to compete on specialty pharma. Amgen’s numbers are smaller partly because they’re narrower—mainly oncology and immunology.

The top four are all within $5 billion of each other. That wasn’t true a decade ago. It’s more competitive now.

Lilly’s position is built on GLP-1s, which are hot right now but won’t be novel forever. Pfizer still has COVID money coming in. AbbVie and J&J have older businesses that are more stable.

In a few years, when the trends shift, you’ll see who actually built something versus who just caught the wave.