The Indian paracetamol market is one of the most resilient and essential segments of the country’s pharmaceutical landscape. Valued at $1.36 billion in 2024, the market is projected to grow to $1.75 billion by 2030 at a compound annual growth rate (CAGR) of 4.46%.

This growth is fueled by a massive population base, increasing health awareness, and the entrenched habit of self-medication for common ailments like fever and musculoskeletal pain.

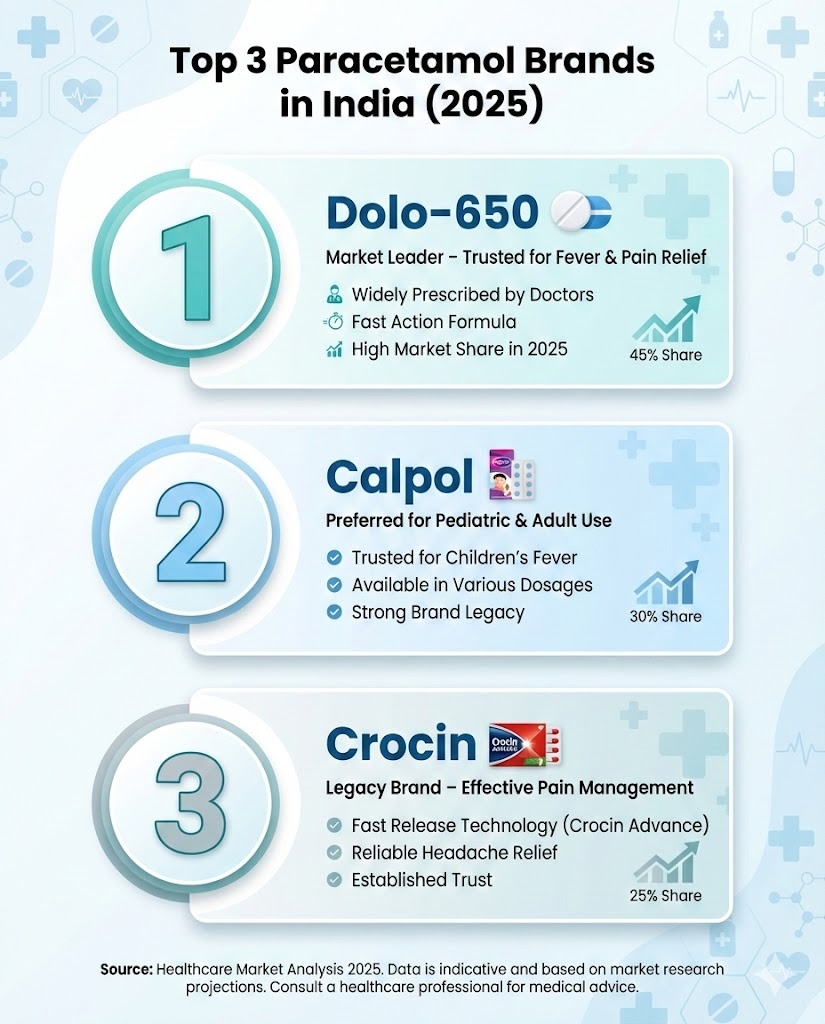

Market Leaders: The “Big Three”

While thousands of generic versions exist, the retail and prescription space is dominated by a few flagship brands.

- Dolo-650 (Micro Labs Ltd): Cementing its role as “India’s national tablet,” Dolo-650 commands 50% of the 650mg paracetamol segment as of July 2025. It recorded sales of ₹311.7 crore in the 12 months ending July 2025 and remains the most prescribed brand in the country.

- Calpol (GSK Pharmaceuticals): The primary challenger to Dolo, Calpol recorded sales of ₹135.4 crore in the same period. It maintains a dominant position in pediatric formulations and is highly trusted by healthcare professionals.

- Crocin (GSK Pharmaceuticals): A household name with massive universal recall, Crocin leads the over-the-counter (OTC) segment. During the pandemic, it saw sales growth as high as 53%, further solidifying its presence in home medicine cabinets.

Manufacturing and Global Hub Status

India is not just a consumer but a global production powerhouse for paracetamol.

- API Production: In 2024, India produced 43,000 metric tonnes of paracetamol Active Pharmaceutical Ingredient (API).

- Leading Manufacturers: Granules India Ltd is a global titan, controlling approximately one-third of the world’s paracetamol API volume with plans to reach 50% by 2027. Other key players include Farmson Pharmaceuticals, which produces about 22% of global demand, and Meghmani LLP.

Key Market Trends for 2025-2026

- Segment Shift: The 500mg variant still holds the largest overall market share at 60.75%, though 650mg doses have seen rapid adoption since the COVID-19 pandemic.

- Distribution Evolution: Retail pharmacies remain the primary channel, holding over 52% market share, but online pharmacies are the fastest-growing segment with a projected CAGR of nearly 5%.

- Formulation Innovation: While tablets lead with a 46.18% revenue share, injectable formulations (IV) are growing at 4.78% as hospitals seek rapid-onset solutions for pain and fever.

Despite challenges such as raw material price fluctuations and intense competition from budget generics (which can be up to 37% cheaper than leading brands), India’s paracetamol market continues to expand as it transitions from a pandemic-driven surge to steady, long-term growth.