In an era where artificial intelligence (AI) is reshaping economies, societies, and daily life, the physical backbone of this transformation remains surprisingly tangible: data centers. These massive facilities house the servers, storage systems, and networking equipment that power everything from cloud computing and streaming services to advanced AI training models that require immense computational power. As AI adoption accelerates globally, countries are scrambling to expand their data center capacity to meet surging demand for low-latency processing, data sovereignty, and digital resilience.

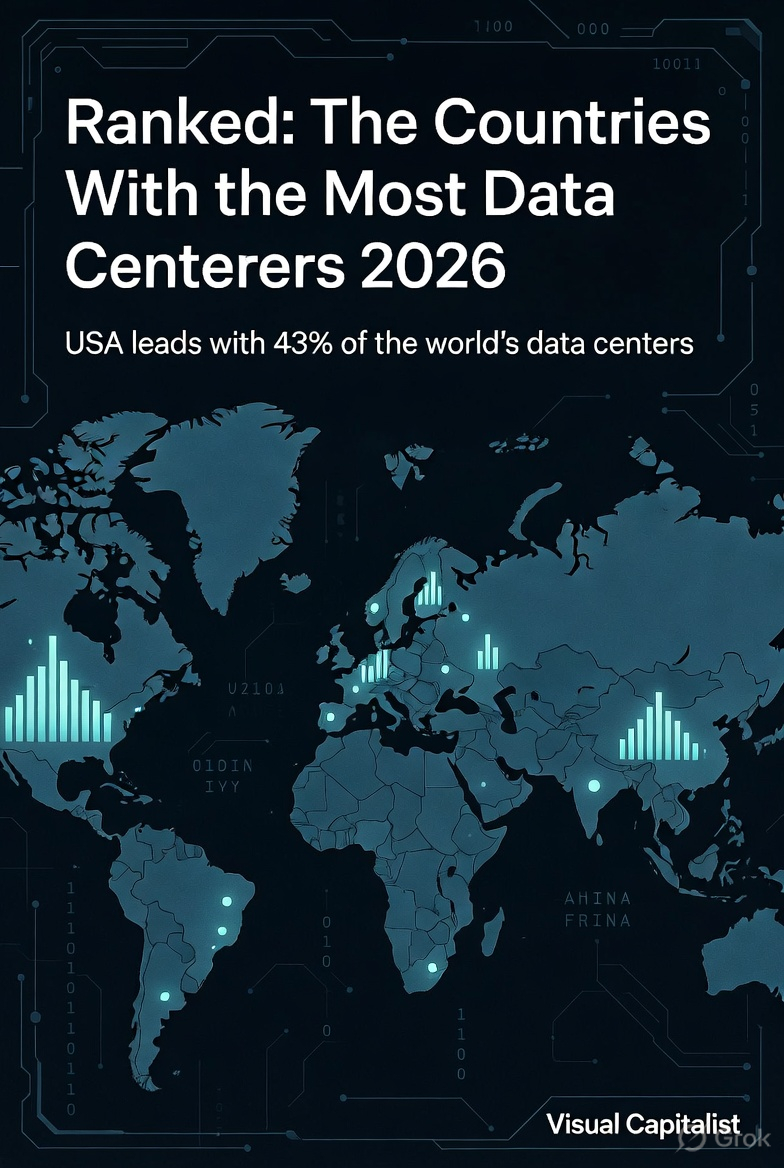

According to the latest data from Data Center Map as of March 2026, the world’s data center landscape is highly concentrated, with a handful of nations dominating the infrastructure that underpins the digital economy. The United States alone accounts for a staggering 43% of global data centers, totaling 4,088 facilities. This dominance reflects not only the presence of tech behemoths like Amazon, Microsoft, and Google but also the country’s vast land availability, relatively favorable energy markets in certain regions, and mature ecosystem of hyperscale operators. Yet, the race is far from over. Europe’s traditional hubs are holding strong, while emerging markets in Asia and beyond are rapidly scaling up. This article dives deep into the rankings, analyzes the drivers behind national strengths, explores regional hotspots, examines construction booms and bottlenecks, and looks ahead to the future of this critical infrastructure amid AI-driven growth, energy constraints, and sustainability challenges.

Global Rankings: The Uneven Distribution of Digital Powerhouses

The treemap visualization from Visual Capitalist, based on March 2026 figures, paints a clear picture of concentration. Here is the top 15 breakdown:

- 1. United States: 4,088 data centers

- 2. Germany: 507

- 3. United Kingdom: 506 (just one behind Germany)

- 4. China: 369

- 5. France: 346

- 6. Canada: 286

- 7. India: 278

- 8. Australia: 270

- 9. Japan: 255

- 10. Italy: 216

- 11. Brazil: 204

- 12. Spain: 195

- 13. Netherlands: 187

- 14. Indonesia: 185

- 15. Russia: 181

At the other end of the spectrum, smaller nations like Belarus (2 facilities), Monaco, and Azerbaijan (3 each) underscore how data center development correlates strongly with economic size, technological maturity, and population density in developed or rapidly digitizing economies. AI penetration is highest in advanced nations, so it is no surprise that data centers cluster where end users, enterprises, and financial markets demand ultra-fast connectivity.

The United States’ lead is overwhelming—more than eight times the number of the runner-up. This isn’t just scale; it’s strategic. American data centers support hyperscale cloud providers serving global clients, while domestic demand from AI startups, government agencies, and enterprises continues to explode. Proximity to users matters: low latency is non-negotiable for real-time AI applications like autonomous vehicles, financial trading algorithms, and personalized healthcare analytics.

Europe follows closely as a collective powerhouse. Germany and the United Kingdom are nearly tied, reflecting their roles as economic anchors in the European Union and beyond. Germany’s position benefits from its central location, robust manufacturing base (Industry 4.0 needs reliable data processing), and strong emphasis on data privacy under GDPR. The United Kingdom, post-Brexit, has positioned itself as a fintech and AI innovation hub, with London drawing massive investment.

The FLAP-D corridor—Frankfurt, London, Amsterdam, Paris, and Dublin—remains Europe’s undisputed epicenter for cloud and AI infrastructure. These cities offer dense fiber networks, proximity to major financial markets, skilled talent pools, and regulatory stability. France (346 facilities) slots in just behind China, benefiting from Paris’s role in the corridor and national policies promoting digital sovereignty. The Netherlands and Spain also rank respectably, leveraging Amsterdam’s connectivity and Spain’s growing renewable energy capacity.

Asia presents a mixed but dynamic picture. China (369) is aggressively building to support its domestic tech giants (Baidu, Alibaba, Tencent) and state-driven AI ambitions, though strict data localization rules and geopolitical tensions limit some international hyperscaler involvement. India (278) and Japan (255) are leveraging large populations and growing digital economies—India’s tech outsourcing heritage and startup scene make it a natural fit, while Japan focuses on high-reliability facilities amid earthquake risks. Australia (270) stands out for its vast land and stable politics, serving as a regional hub for Oceania and Southeast Asia.

Latin America and other emerging regions show promise but lag. Brazil (204) leads in South America thanks to its size and economic weight, while Indonesia (185) benefits from a young, digitally native population driving e-commerce and mobile-first services. Russia (181) maintains a notable presence despite sanctions, prioritizing sovereign infrastructure.

Smaller or more remote nations trail because data centers require reliable electricity, high-speed fiber optics, cooling resources, and capital-intensive construction. This creates a self-reinforcing cycle: leaders attract more investment, widening the gap.

Inside the U.S. Boom: States Poised for Dominance

While the national picture is clear, the real action in the United States is hyper-local. A companion analysis from Aterio (March 2026) reveals a dramatic shift in the domestic pipeline when factoring in operational sites, projects under construction, and announced developments. Texas is set to overtake traditional leader Virginia, with a projected total of 962 data centers (212 operational, 140 under construction, and a massive 610 announced). Virginia currently leads with 320 operational and 954 in the total pipeline, but Texas’s land availability, lower energy costs in certain grids, and business-friendly policies are accelerating its rise.

Georgia emerges as a breakout star: its 340 announced projects alone dwarf its current 62 operational facilities—a more than 5x multiplier. Pennsylvania, Arizona, Ohio, and Illinois are also surging, with total pipelines exceeding 250 each. California, despite its tech concentration (166 operational), ranks lower in future growth due to high land costs, strict regulations, and grid constraints.

This state-level race is driven by practical factors. Access to affordable, reliable power is the single biggest constraint. Developers increasingly seek disused industrial “brownfield” sites with existing grid connections to bypass permitting delays. Construction timelines average around two years, but hyperscale projects can stretch longer depending on size and approvals. Announced projects—identified via building permits, utility filings, or public announcements—signal intent but require ground-breaking to move into the “under construction” category.

New Hampshire, the District of Columbia, Rhode Island, Hawaii, and Vermont currently have zero projects under construction or announced. Several states, including Vermont and New Hampshire, are even considering moratoriums or restrictions on new builds due to concerns over energy strain, water usage for cooling, and local community impacts.

The AI Imperative: Why Capacity Is Exploding Now

The surge is no accident. AI applications are voracious consumers of compute. Training large language models or running inference at scale demands thousands of GPUs operating continuously, generating heat and requiring constant power. Low latency means facilities must be built closer to users—hence the global push beyond traditional hubs.

This boom coincides with broader tech industry shifts. A separate Visual Capitalist ranking of disclosed tech layoffs in 2025 and early 2026 (data from Layoffs.fyi as of March 16, 2026) shows Amazon leading with 30,184 cuts, followed by Intel (27,058) and Microsoft (15,347). These three alone account for roughly 64% of tracked layoffs among major firms. While counterintuitive amid infrastructure growth, the pattern reflects efficiency drives: companies are streamlining management layers, automating routine tasks with AI (as Block’s CEO explicitly noted), and reallocating resources toward high-priority AI investments. Amazon, for instance, cited reducing bureaucracy to speed decision-making while still hiring selectively in growth areas. Intel framed its cuts as part of a multiyear turnaround to align costs with new operating models.

In short, the industry is optimizing human capital to fund the machines that will power the next wave of innovation.

Challenges on the Horizon: Power, Land, Water, and Sustainability

Finite resources pose serious headwinds. Data centers are energy hogs—some hyperscale facilities consume as much electricity as entire small cities. Cooling accounts for a huge portion of usage, raising water stress concerns in arid regions. Land scarcity in prime metropolitan areas forces developers farther afield or into creative solutions.

Positive examples of community integration are emerging. In Ireland, which lifted a data center moratorium late last year, an AWS facility now feeds excess heat into a district heating network serving social housing and public buildings—turning a potential waste product into a public good. Such co-benefits help secure local buy-in and regulatory approvals.

More radical innovations are on the drawing board. Some developers are exploring orbital data centers to bypass terrestrial constraints entirely, leveraging space-based solar power and radiative cooling in vacuum conditions. While still conceptual, China’s moves in this direction signal serious interest.

Geopolitics adds another layer. Data localization laws, export controls on advanced chips, and concerns over foreign ownership mean nations are treating data centers as strategic assets akin to energy or telecommunications infrastructure. Supply chain risks for critical minerals (copper, rare earths, and semiconductors essential for servers and GPUs) further complicate expansion, as highlighted in related analyses of AI’s material demands.

Economic and Geopolitical Implications

The data center race is reshaping global economics. Countries with robust capacity gain advantages in attracting AI talent, fostering innovation ecosystems, and capturing tax revenue from hyperscalers. The U.S. and Europe currently lead, but Asia’s rapid scaling could shift the balance. Emerging markets like India and Indonesia stand to benefit from leapfrogging legacy infrastructure, much as they did with mobile networks.

For businesses, reliable local data centers mean lower latency, better compliance, and resilience against outages or geopolitical disruptions. Insurers and risk managers (noting partnerships like those highlighted in geopolitical risk coverage) are increasingly pricing in data center concentration risks—single points of failure in the digital supply chain could have cascading effects on global markets.

Looking Ahead: The Next Phase of the Buildout

Projections suggest the boom is only beginning. AI demand shows no signs of plateauing, and generative AI tools are proliferating across industries. By 2030, global data center power consumption could rival that of entire countries today. Solutions will include renewable energy co-location (solar and wind farms dedicated to facilities), advanced cooling technologies (liquid immersion, free-air cooling), and modular, prefabricated designs to speed deployment.

Policy will play a decisive role: incentives for green data centers, streamlined permitting, and international cooperation on standards could accelerate sustainable growth. Conversely, fragmented regulations or energy shortages could throttle progress in key markets.

In conclusion, the 2026 data center rankings reveal a world racing to build the foundations of an AI-powered future. The United States remains the undisputed leader, but Europe’s FLAP-D corridor, China’s domestic focus, and rising stars like Georgia and Texas illustrate a diversifying landscape. Challenges around energy, sustainability, and geopolitics will test even the strongest players, yet the rewards—economic competitiveness, technological sovereignty, and societal advancement—are immense. As developers innovate and communities negotiate trade-offs, the data center map of tomorrow will look markedly different from today’s. The infrastructure being laid now will determine which nations thrive in the intelligence age.