When Eli Lilly crossed a $1 trillion market capitalization, many observers framed it as a sudden success driven by obesity drugs. In reality, the milestone reflects one of the fastest and most disciplined strategic pivots in modern pharmaceutical history.

Just five years ago, Lilly still looked like what it had been for decades: an insulin-centric diabetes company with a diversified but aging portfolio. Today, it stands as the global leader in the incretin era, reshaping not just its own revenue mix but the future of metabolic medicine.

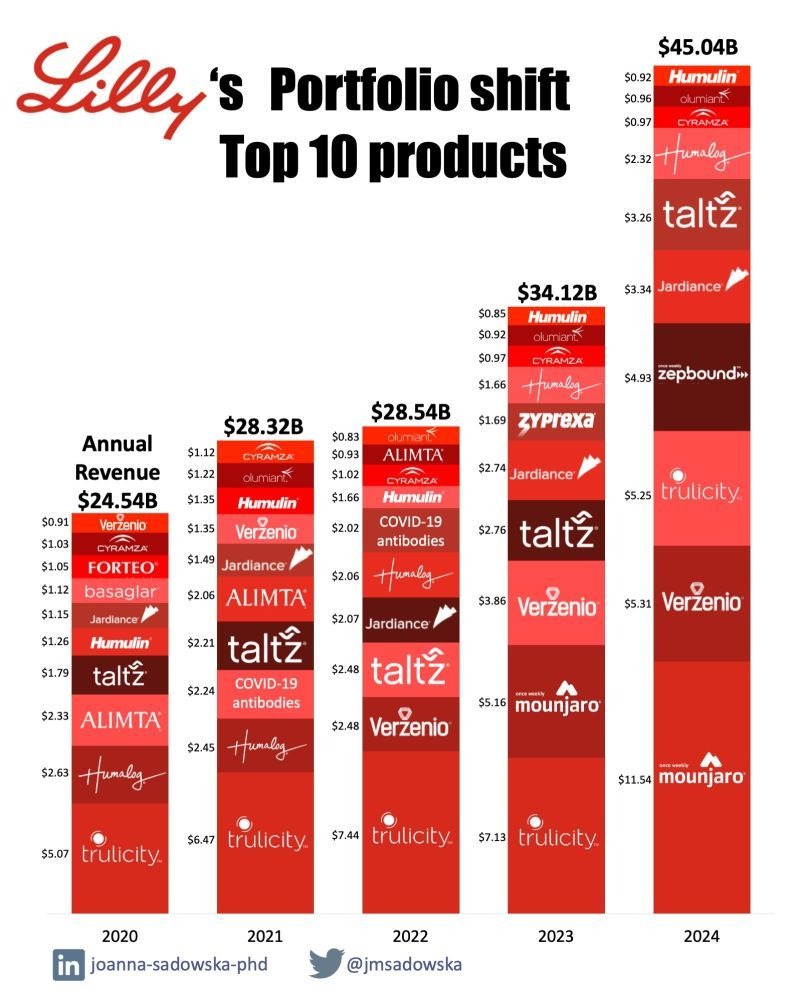

The shift is visible in the data — and the scale is striking.

From Stability to Reinvention

In 2020, Lilly’s top 10 products generated roughly $24.5 billion in annual revenue. Much of that came from:

-

Legacy insulins (Humulin, Humalog)

-

Mature oncology assets (Alimta)

-

A broad diabetes portfolio with limited growth prospects

These products were reliable but constrained. Pricing pressure, biosimilar competition, and market saturation made long-term growth increasingly difficult.

Instead of defending the past, Lilly began engineering an exit from it.

Managing Decline While Funding the Future

What makes Lilly’s story unusual is not that legacy products declined — that’s inevitable in pharma — but how cleanly the company managed that decline.

Older diabetes franchises were gradually harvested rather than abruptly abandoned. Cash flows were preserved and redirected into:

-

Incretin science

-

Manufacturing scale

-

Commercial infrastructure capable of supporting global chronic therapies

This allowed Lilly to avoid the revenue cliffs that often accompany major portfolio transitions.

Trulicity: The Bridge Drug

For much of the 2020–2023 period, Trulicity was the anchor of Lilly’s growth:

-

It became the company’s largest product

-

It familiarized physicians with GLP-1 biology

-

It built commercial expertise in metabolic disease at scale

Crucially, Trulicity was never treated as the end state. It was a platform builder, not the final act.

The Obesity Inflection Point

The real transformation arrived with tirzepatide.

By 2023–2024:

-

Mounjaro emerged as Lilly’s largest single product

-

Zepbound rapidly expanded the franchise into obesity

-

Combined, these products generated over $16 billion in 2024 alone

This wasn’t incremental growth — it was a category reset. Lilly moved from competing in diabetes to owning the metabolic disease narrative, spanning diabetes, obesity, and cardiometabolic risk.

Meanwhile, total top-10 product revenue nearly doubled to ~$45 billion in five years.

Why the Market Responded So Strongly

Lilly’s valuation surge isn’t driven only by current sales. Investors are pricing in:

-

Long-duration chronic use

-

High patient retention

-

Follow-on pipeline assets

-

Manufacturing capacity as a competitive moat

-

Category leadership in a market measured in hundreds of billions, not tens

Few pharma companies control an entire therapeutic paradigm. Lilly increasingly does.

A Rare Strategic Outcome

Pharma pivots are slow, risky, and often painful. Lilly executed one at exceptional speed by sequencing its moves correctly:

-

Preserve legacy cash flows

-

Scale a transition product

-

Launch a category-defining platform at exactly the right moment

The result is not just a stronger company, but a fundamentally different one.

The Bigger Lesson

Eli Lilly’s rise shows that true transformation in pharma doesn’t come from chasing trends — it comes from building platforms early and having the patience to let science, manufacturing, and markets align.

In five years, Lilly didn’t just grow faster.

It changed what kind of company it is.

And the market noticed.