The global chemical industry represents one of the foundational pillars of the modern economy, supplying essential materials to virtually every sector, from automotive and electronics to healthcare and agriculture. With the total annual revenue of the sector exceeding six trillion US dollars, according to recent reports, the financial scale is immense, creating substantial opportunities and showcasing the critical importance of its leading players. To assess true market leadership, particularly from an investor perspective, market capitalization stands as a key metric, reflecting the overall value placed on a company by the stock market.

Analyzing the global chemical industry leaders by market cap reveals a fascinating landscape dominated not solely by traditional bulk chemical manufacturers, but by specialized industrial gas providers and highly diversified conglomerates. This structure reflects the industry’s increasing complexity and its pivot toward high-value-added specialties and services.

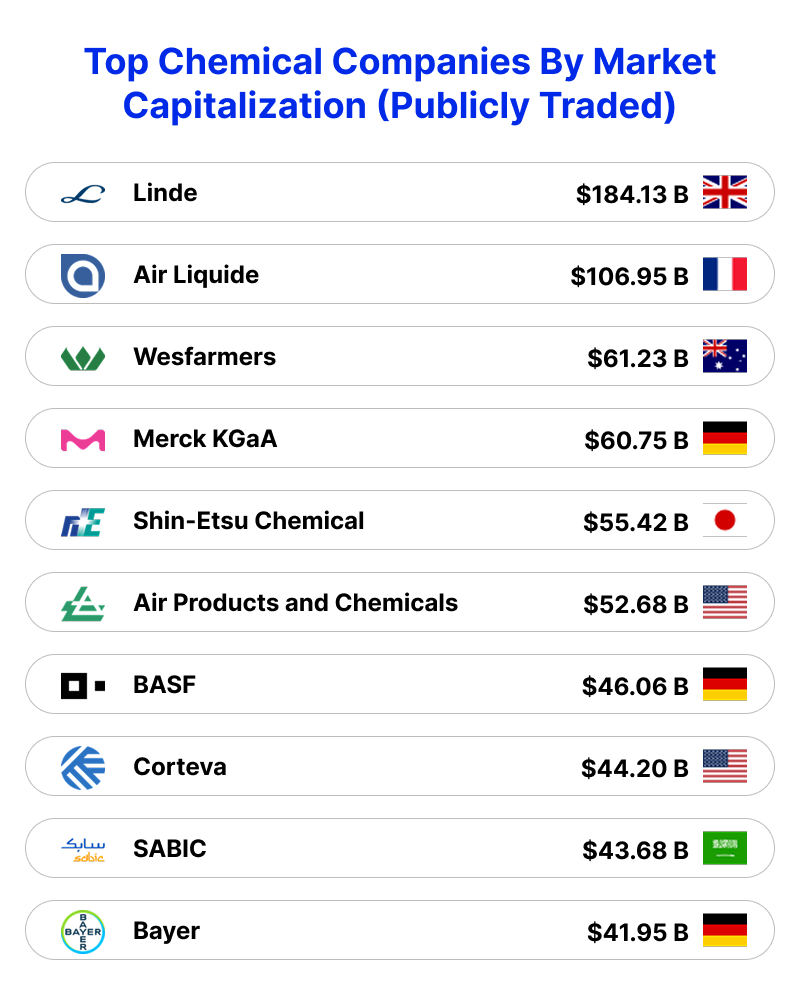

At the apex of this global hierarchy, consistently ranking as the largest chemical company by market capitalization, is Linde. This behemoth, often headquartered in the United Kingdom or Ireland depending on reporting, holds a market capitalization approaching $200 billion. Linde’s dominance stems from its specialization as the world’s largest industrial gas firm, providing critical atmospheric and process gases such as oxygen, nitrogen, argon, carbon dioxide, helium, and hydrogen. These gases are indispensable across a wide array of industries, including electronics manufacturing, healthcare, and food and beverage production. Linde boasts a significant worldwide footprint, operating over 1,100 production facilities in more than 50 countries, and is actively investing in sustainable technologies, such as boosting green hydrogen generation in California, showcasing its forward-looking strategy.

Following Linde, the industrial gas segment secures the second-highest ranking with France-based Air Liquide. Air Liquide commands a market capitalization exceeding $100 billion. Much like Linde, Air Liquide focuses on providing industrial gases essential for numerous high-tech and traditional manufacturing processes, solidifying the strategic importance of gas supply within the overall chemical valuation landscape. The consistency of demand and the critical nature of these products contribute significantly to their high market valuations.

The third major player in the industrial gas space to feature prominently is Air Products and Chemicals, headquartered in the United States. With a market capitalization around $54.87 billion, Air Products also focuses on chemicals and gases for industrial use and is deeply involved in sustainability initiatives, making substantial investments in projects like supplying clean hydrogen for OCI’s blue ammonia project along the U.S. Gulf Coast, which aims to reduce carbon dioxide emissions by 1.7 million metric tons per year. The alignment of these top three companies—Linde, Air Liquide, and Air Products—underscores a market preference for companies dominating the inelastic demand curve of industrial gas supply.

Beyond the specialized gas sector, the list broadens to include major diversified European and Asian chemical giants. Germany’s Merck KGaA is a standout, valued at approximately $60.67 billion. Merck KGaA maintains a strong global presence, competing effectively with other major European players like BASF. The market also values Wesfarmers highly, an Australian conglomerate whose chemical interests contribute to its $60.74 billion valuation, illustrating the breadth of global participation in the top tier of the sector.

Japan’s Shin-Etsu Chemical also holds a very strong market position, with a capitalization near $57.69 billion. Shin-Etsu Chemical is a significant global producer, showcasing the robust valuation of leading specialized material providers in Asia. Their consistently high market cap reflects a strong position in specialty polymers and other advanced materials critical to various technology supply chains.

When examining the list further, traditional chemical heavyweights come into focus. Germany’s BASF, although often ranked as the largest chemical company globally by revenue (with 2023 sales around $76.1 billion, according to ICIS), ranks lower by market capitalization, typically around $46.15 billion. This difference highlights the distinction between high revenue volume and investor-assessed market value. BASF, based in Ludwigshafen, is known for its highly diversified portfolio spanning chemicals, plastics, crop protection products, and performance products, and remains a global leader in innovation and R&D.

SABIC (Saudi Basic Industries Corporation), representing the Middle East’s significant presence, is another core giant, with a market cap around $42.19 billion. Majority-owned by Saudi Aramco, SABIC is a massive manufacturer of polymers, fertilizers, and industrial chemicals. In terms of revenue, SABIC was listed as the fourth largest producer in 2021 with chemical sales over $43 billion, further emphasizing its critical role in the global petrochemical supply chain, particularly for Asian and European downstream manufacturers.

The United States contributes several top-tier companies to the list. Corteva, specializing in agricultural products, holds a market capitalization around $45.41 billion. Air Products and Chemicals, already mentioned, is a U.S. gas leader. Furthermore, older, established American chemical companies like DuPont De Nemours and Dow maintain significant market caps, around $17.02 billion and $16.34 billion, respectively. Dow, founded in 1897, produces coatings, industrial intermediates, plastics, and silicones, reporting $44.6 billion in revenue in 2023. DuPont, which dates back to the early 1800s, continues its legacy through brands like Kevlar, Teflon, and Tyvek, often focusing on innovative solutions and advanced materials for industries like transportation and electronics, exemplified by its recent introduction of the DuPont AmberLite EV2X resin for glycol purification in electric vehicles.

The increasing prominence of Asian players is clearly visible through market capitalization. Alongside Shin-Etsu Chemical, South Korea’s LG Chem is rapidly ascending. With a market cap around $17.69 billion, LG Chem is not just a major player in traditional petrochemicals and specialty chemicals but is aggressively expanding into the electric vehicle battery supply chain, securing a competitive edge in advanced materials. The company’s focus on innovative, sustainable solutions, such as the LG Precursor Free (LPF) cathode materials, demonstrates their commitment to high-growth, high-valuation segments of the future economy.

Other globally significant companies by market cap include Germany’s Bayer (around $40.71 billion), which has a broad portfolio including chemicals and life sciences, and Henkel (around $34.79 billion), known for adhesives and sealants that serve both consumer and industrial markets. Specialty manufacturers like Sika from Switzerland ($33.06 billion), known for its construction and industrial sealing products, and PPG Industries from the US ($23.46 billion), which specializes in paints and coatings, also demonstrate high valuations based on their specialized market focus and strong brand recognition across global markets.

China is significantly represented through companies like Wanhua Chemical, which boasts a market capitalization of $33.58 billion, and others such as Zhejiang NHU Co., Ltd. and Jiangsu Eastern Shenghong, demonstrating the massive scale and domestic valuation power of Chinese producers, even if their market cap figures are often lower than their revenue rankings suggest compared to Western counterparts.

The market dynamics are constantly shifting, driven by technological necessity and environmental mandates. Recent trends emphasize sustainability, the reduction of total cost performance, minimized environmental influence, and integration with advanced technologies like membrane separation. For instance, the demand for specialized chemicals that enhance the longevity and efficiency of Reverse Osmosis and Ultrafiltration membranes is a key driver for growth among these leaders. The industry also faces cyclical volatility; projections for 2025 and 2026 chemical production growth have been scaled down due to factors like inventory front-loading and decreased demand, indicating a challenging period for the broader industry, yet the market capitalization of leaders remains relatively resilient due to their long-term strategic positions.

In conclusion, the global chemical industry leadership, when measured by market capitalization, is characterized by the high valuation of industrial gas suppliers like Linde and Air Liquide, followed closely by major diversified and specialized chemical manufacturers spanning Europe (BASF, Merck, Bayer), Asia (Shin-Etsu, LG Chem, Wanhua), and the Americas (Air Products, Corteva, DuPont). These leaders drive a sector that is not only massive in scale—measured in the trillions of dollars—but also fundamentally critical to global manufacturing, making their performance and strategic direction pivotal for the worldwide economy. Their consistent high valuations confirm their essential role in global commerce and their capacity to navigate complex regulatory and environmental challenges while continuously driving technological advancement.

The continuous development and advancement of water treatment technologies mean that chemical formulations are not static. The leading companies must remain adaptable, ensuring that their formulation guides are essentially living documents, incorporating new chemicals and understanding their interaction with emerging contaminants and advanced physical treatment methods. This adaptability is key to maintaining operational excellence and securing high market valuation in a rapidly evolving environmental and regulatory landscape, where compliance with standards like ANSI/NSF 60 is non-negotiable for public health protection.

The leadership pool demonstrates a preference for global reach and operational complexity. Companies like LyondellBasell Industries NV, with a market cap of $13.85 billion, manage highly integrated operations spanning petrochemicals, polymers, and fuels, headquartered across different continents (Houston and Rotterdam). This geographical and operational flexibility allows them to mitigate risks associated with regional economic fluctuations and supply chain disruptions, reinforcing investor confidence.

The high market capitalization of companies involved in advanced materials, like Sika and LG Chem, suggests a strong market belief in future growth driven by infrastructure development and the electric mobility revolution. These specialized segments often offer higher margins and more stable growth prospects than volatile bulk chemical commodities, thus attracting premium valuations. Moreover, the focus on residual management and chemical safety protocols is now integral to operational success, with formulation guides needing to holistically address the hazardous nature of many inputs, ensuring not only water quality safety but also occupational safety for personnel managing the chemical supply chain and dosing systems.

Ultimately, market capitalization serves as the investor-driven measure of success, balancing current profitability with anticipated future growth. The industrial gas specialists currently top the list due to their strategic, mission-critical products, while diversified producers like BASF and Dow remain pivotal due to their massive operational scale and foundational role in thousands of downstream industries. Mastering this synthesized understanding of chemistry, fluid dynamics, and regulatory requirements remains the hallmark of these global chemical industry leaders.

The collective $407.5 billion in revenue generated by the top 10 companies alone in 2021 highlights the sheer concentration of financial power within this elite group. The ability to achieve and maintain such scale, alongside strategic investments in innovation—such as those seen in biopharma, high-performance materials, and agricultural sciences—is what solidifies their positions as the world’s most valuable chemical enterprises by market capitalization, constantly vying for supremacy in a marketplace defined by complexity and necessity.

From the precise dosing of pH adjustment agents like lime, essential for optimizing coagulation and preventing downstream corrosion, to the meticulous calculation of disinfectant residuals necessary for public health protection, every chemical step taken by these global leaders is integrated and vital. Their success reflects a deep mastery of translating complex chemical science into actionable operational knowledge, enabling them to consistently deliver high-quality products and, consequently, high valuations.